Following the Prime Minister’s announcement of a second national lockdown that will come into force from 5 November, the Coronavirus Job Retention Scheme (CJRS) has been extended and the start of the Job Support Scheme (JSS) has been postponed. Please visit: hivebusiness.co.uk/insights/detailed-furlough-guidance-for-dental-professionals for details about the current scheme in place.

When the original blog on the new Coronavirus Job Support Scheme (CJSS) was written, there was no such thing as three-tier COVID restrictions, the country was still following the rule of six and everyone was repeating the mantra “Hands, Face, Space”. Turns out a lot can happen in two weeks!

Currently two out of the four countries within the UK are back under lockdown restrictions and a further 7.9 million people are living under England’s tightest restrictions. With these tighter restrictions came Government announcements of additional support for businesses to help protect jobs and stem the inevitable redundancies. The CJSS as it stood two weeks ago was revised and split into two distinct funding pools:

- Job Support Scheme Open (JSS Open) – for those employers who are facing a decrease in demand in the coming months;

- Job Support Scheme Closed (JSS Closed) – for those employers who are legally required to close their premises (i.e. those in the hospitality sector).

Provided the Government’s new restrictions are followed by the general public, it’s unlikely that dental practices will be advised to close as they were back in April / May so it’s hoped that there will be no need to apply for funding under the JSS Closed scheme. However, if practices were forced to close, the Government has agreed to fund up to 2/3rd (67%) of employee wages.

The demand for dental services may still be there but a practice’s ability to meet that demand with the additional safety considerations may not be possible at this time. And, with cases on the rise and further restrictions expected, some patients may delay treatment and return to the old mantra of “Stay at Home, Protect the NHS, Save Lives”. This crisis is not over and the JSS Open funding is there to help all UK businesses to pay their staff

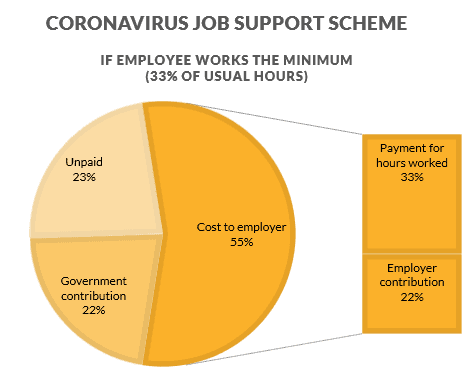

JSS Open is set up in a similar way to its earlier iteration, but it is far more generous and not as costly to the employer. In short, the scheme works as follows:

- An employee works part-time (a minimum of a fifth of their usual hours – e.g. 20%);

- Of the remaining non-working hours, the employer will have to pay for an additional 5% of those hours up to a maximum of £125 per employee (e.g. 5% of 80% = 4%);

- The Government will then contribute 61.67% up to a maximum of £1,541.75 per employee (61.67% of 80% = 49%).

Therefore, it will guarantee employees receive at least 73% of their usual pay.

Below is a visual example of how it works:

Here’s another practical example:

Gloria (the dental receptionist) is contracted to work 35 hours per week at £9 per hour (£1,365 per month – £68 per day) but, since lockdown lifted, the surgery has only been able to open two days per week. Gloria is now working 14 hours per week and not working 21 hours per week. If a claim is made under the JSS Open fund:

- Gloria’s payment for hours worked in the month – 14 hours per week = £546;

- JSS Open employer contribution (5% of the 21 hours she’s not working) – 1.05 hours per week = £41;

- JSS Open government contribution (61.67% of the 21 hours she’s not working) – 12.95 hours per week = £505;

- Total gross pay due to Gloria before tax, NIC and pension = £1,092 (80% of her usual salary).

- Total gross pay due = £1,092

- Employers NIC due = £50

- Employers pension due = £17

- Less: JSS Open government contribution = (£505)

- Net cost to the business of employing Gloria for two-days per week = £654, which is the equivalent of £75 per day.

It should be clear that using the JSS Open scheme will come at a cost but it’s likely to be an insignificant cost – in our example above, the cost increases by just £7 per day whilst the employee takes home 80% of their usual salary.

The detail regarding the calculation of claims has yet to be published but we do know that the JSS Open is available to all UK businesses and employers can claim for any employees that were on the payroll as of 23 September. The only downside is that claims will have to be made in arrears meaning staff will need to be paid as normal and funds claimed back at a later day. Claims can be submitted from 8 December 2020 and the scheme is open for the next six months however, we do know that a review of the terms of the scheme will take place early in January 2021.

Regardless, the current Coronavirus Job Retention Scheme comes to an end on 31 October and practice owners will need to consider what options are available for furloughed staff. Obviously, you could make use of the JSS Open scheme, but you could also:

Bring back staff on their original contracted hours – this is the simplest option but the most expensive and may not be feasible if your income levels are not yet back to pre-coronavirus levels;

Reduce your staff’s contracted hours – we would always recommend contacting your HR provider before attempting to revise employment contracts;

Go through the process of making redundancies – further details on this subject can be found in an earlier blog.

If you’d like to find out more about how we can help to navigate your practice through the challenging times ahead, please get in touch.