By Connor Smith, Accountant at Hive Business

Undoubtedly, one of the more controversial changes to tax law in recent years has been the restriction of how much pension contributions can be made each year by high earners. This controversy is perhaps only compounded by the fact that the calculation for working out how much you need to adjust the allowance by seems to have been so devilishly designed by HMRC that only Issac Newton himself would have any chance of understanding it. The result is unhappy taxpayers, unhappy advisors and, perhaps unsurprisingly, a very smug HMRC.

Why has it been introduced?

It was a move viewed by some as HMRC attempting to take away some of the advantages that the wealthy with excess cash could utilise. Those with the cash and resources available could, in theory, contribute up to £40,000 each year into their personal pension pots, saving for their (already likely secure) future whilst also saving a whole heap of tax, regardless of how much they earn.

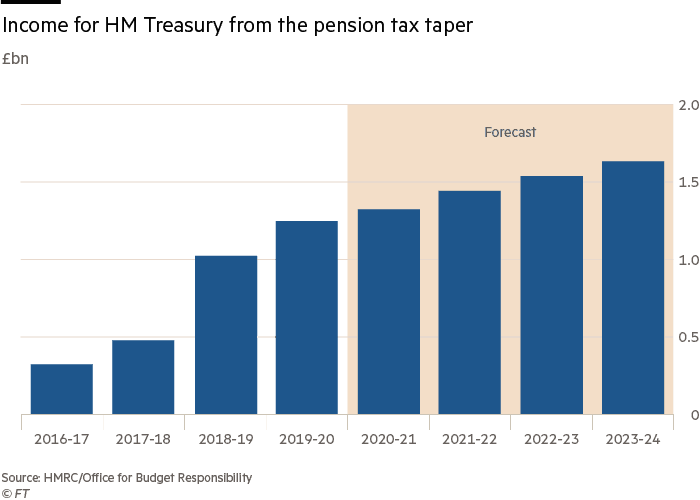

Whilst the taper has been described by former pensions minister Steve Webb as ‘utterly absurd’ for the impact it’s having on the public sector, HMRC is unlikely to reverse the rules anytime soon, due to the potentially huge tax bonus they receive from taxpayers being caught out. Fiscal projections alone from the Office for Budget Responsibility predict that tax receipts as a result of the changes are likely to be in excess of £1.5bn for the 2023-24 financial year.

Who has been hit?

The biggest group affected by these changes to have hit the headlines earlier this year is NHS workers, as not only do your own pension contributions count toward this taper, but also those of your employer. Suddenly, doctors putting in overtime found themselves more out of pocket than if they’d turned down the offer of overtime in the first place. The changes are only just now being felt in their full impact, as people previously had the grace of unused allowances brought forward from earlier years to offset against the new rules.

It would, however, be incorrect to assume that only NHS doctors are being hit by these restrictions. Any individual with a high personal income looking to make pension contributions now needs to think carefully about the amount they are putting into their pot.

What can you do?

We no longer operate in a tax world where things can be viewed retrospectively, at the end of the year, with little thought or planning. Setting up a simple standing order to a pension provider and not reviewing your financial affairs pro-actively now comes with a potentially hefty penalty and a liability that could have been avoided.

Previously, the work of an IFA and the work of the accountant have been viewed as two separate and distinct services, despite all linking together into your long term financial position. Now, more than ever, it is absolutely crucial that you need to be working closely on a real-time basis with both advisors to best plan your investments before a decision is made.

At Hive, we are able to provide a full wealth strategy review, and through our network, we are able to refer our clients to trusted financial advisors. Working side by side, we can ensure that your strategy is personalised to your needs, and you aren’t caught by any HMRC horrors at the end of January! If you’d like to discuss your wealth planning, please get in touch.