As a payroll professional and an employee, I’m in a privileged position. I know for sure that every entry on my payslip is correct – the salary, the tax deductions, the pension contributions, everything.

We work closely with our clients to ensure the accuracy of each and every payslip we produce but sometimes an employee will look at their payslip and question what all the deductions are and why they’ve received less cash than they did last month. Below is a brief explanation as to what each payslip entry means and how it is calculated:

Monthly salary

Unless specifically defined in an employee’s contract as a set amount per pay period, employees are usually paid monthly. This is calculated as follows:

Contracted hours per week × Hourly rate of pay × 52 weeks ÷ 12 months

For example:

35 hours per week × £12.00 per hour × 52 weeks ÷ 12 months = £1,820 (salary)

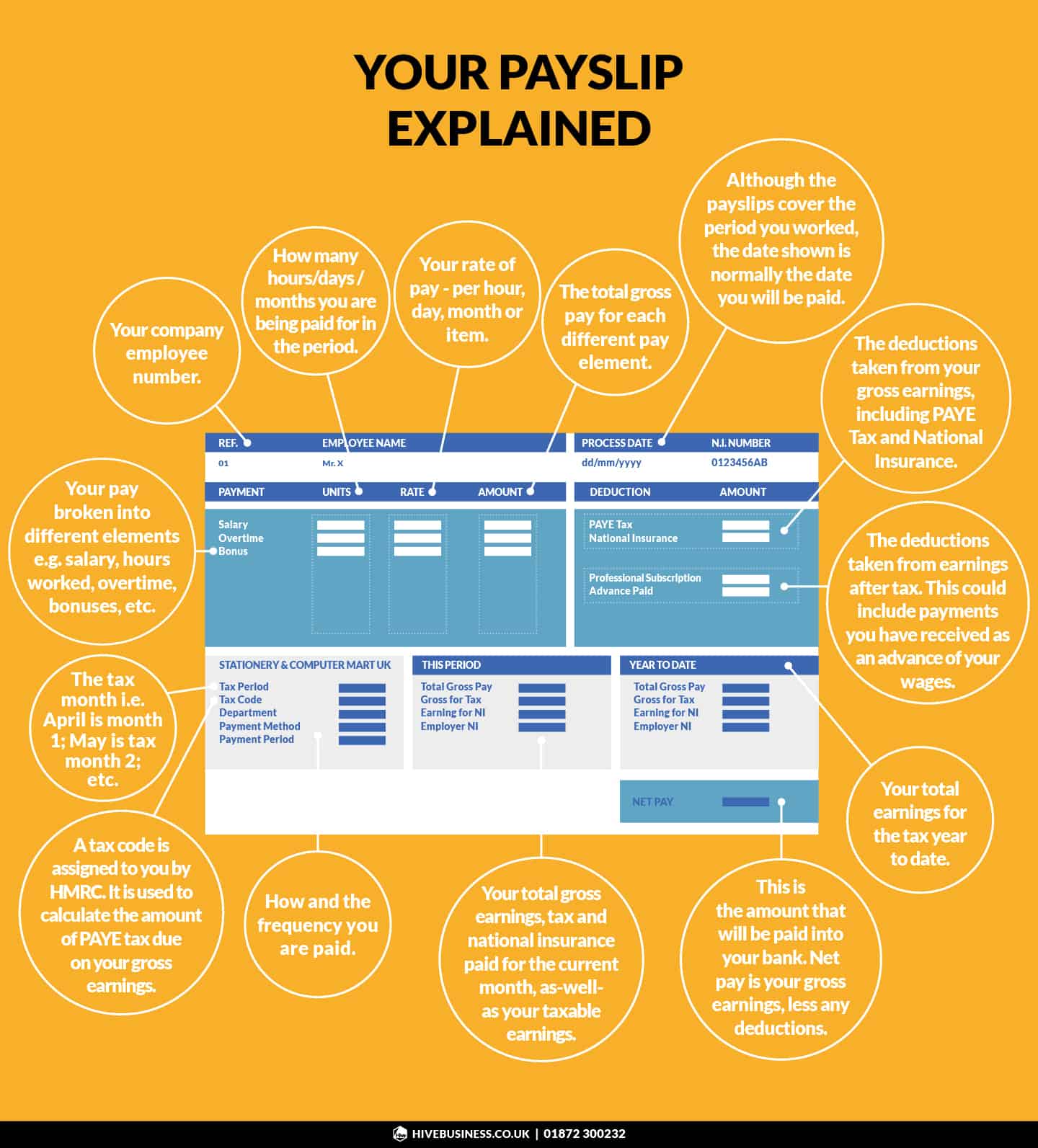

Payslip terms you need to know

Gross pay: Gross salary is the total amount paid to an employee before taxes and other required contributions are subtracted. Your base income plus all benefits and stipends, such as housing, overtime pay, medical insurance, and special stipends, are added up to create this total.

Net pay: Net pay is the term used to describe the take-home pay that employees get after all payroll deductions have been made from their gross pay.

Occupational sick pay vs. statutory sick pay: SSP is a mandatory payment that must be made as long as the employee satisfies the qualifying requirements, whereas OSP is a contractual payment that you choose to provide your employees, giving them an improved entitlement to be paid more than the statutory minimum. SSP for 2023/24 is £109.40 per week.

Statutory maternity pay: This is the statutory minimum that your employer is required to pay you while you are on maternity leave. SMP for 2023/24 is £172.48 per week.

Income Tax

Income tax is used by the Government to “provide funding for public services such as the NHS, education and the welfare system, as well as investment in public projects, such as roads, rail and housing”.

The tax deduction on a payslip is normally based on an employee’s tax code. Every employee has their own code and it’s nearly always made up of some numbers and a letter:

- The numbers refer to how much income you can have before you pay tax;

- The letter refers to the employee’s situation and how it affects their tax-free Personal Allowance.

In the vast majority of cases it’s the number part of the code that is the most important as it sets how much tax an employee will pay.

First, we calculate the employee’s tax-free allowance using their tax code:

Tax code number × 10 ÷ 12 months = Tax-free allowance

For example, if an employee’s tax code is 1257L,they will be able to earn the following amount each month without paying tax:

1257 × 10 ÷ 12 months = £1,048

This tax-free allowance is then deducted from the employee’s salary to give taxable income. The result is multiplied by 20% to give the employee’s tax deduction. For example:

£1,820 (salary) – £1,048 (tax-free allowance) = £772 (taxable income)

£772 × 20% = £154 (tax deduction)

National Insurance

National insurance contributions are paid by both the employee and the employer and are used by the Government to “build your entitlement to certain state benefits, such as the State Pension and Maternity Allowance”.

In 2022, the primary threshold for employee’s national insurance and the personal allowance for income tax were aligned. That means an employee can now earn up to £12,570 without paying any tax or national insurance and hence the NI-free allowance is the same as the tax-free allowance noted in the section above – £1,048 per month.

This NI-free allowance is then deducted from the employee’s salary to give NI-able income. The result is multiplied by 12% to give the employee’s national insurance contribution. For example:

£1,820 (salary) - £1,048 (NI-free allowance) = £772 (NI-able income)

£772 × 12% = £93 (NI deduction)

Auto-enrolment Pension Contribution

For employees earning over £10k per year and aged between 22 and the state pension age, employers are required to automatically enrol them in a workplace pension scheme. Pension contributions are paid by both the employee and the employer and are a way of helping an employee to save up towards their retirement. Contributions are taken and invested in an employee’s own pension pot which can be accessed upon their retirement.

Every year the Government sets out the amount an employee can earn without having to make a pension contribution. For 2023/24, that amount is £520 (pension-free allowance).

This pension-free allowance is then deducted from the employee’s salary to give pensionable income. The result is multiplied by 4% (i.e. 5% after tax relief) to give the employee’s pension contribution. For example:

£1,820 (salary) - £520 (pension-free allowance) = £1,300 (pensionable income)

£1,300 × 4% = £52 (pension contribution)

Net Pay or Take-Home Pay

This is the amount that will land in the employee’s bank account at the end of each month. It’s the amount of salary left after all the items mentioned above are deducted:

Salary – Tax – National Insurance – Pension = Take-home pay

For example:

£1,820 – £154 – £93 – £52 = £1,521 (net pay)

There are other items that could appear on an employee’s payslip (e.g. student loan deductions; attachment of earnings orders) but 99 out of 100 payslips will show all five of these elements.

As you can see there are a lot of calculations involved in payroll. Ensuring the correct deductions are taken from every one of your employee’s pay each month is key to keeping a happy workforce. If you’d like further information regarding our payroll services, please get in touch.

For more info, call us on 01872 300232 or email us at hello@hivebusiness.co.uk.